To My Kids - A Letter From Dad; How To Build Wealth, Avoid Debt, And Buy Your Freedom

To My Kids - A Letter From Dad; How To Build Wealth, Avoid Debt, And Buy Your Freedom

A letter to my kids about how to adult (financially) and live the life of their dreams

Dear kids,

You’re both teenagers now, and I personally think you’ve grown up too fast. Try and work on that, will you?

Up to this point in your lives, your experience with money has been limited to whatever small allowance your mom and I decided to pay you, and perhaps the occasional windfall you received from birthdays or Christmas.

Your relationship with money has been pretty simple:

You either have money and can buy things you want, or

You don’t have money and can’t buy things you want

Managing your money in adulthood is more complicated than that. This post will help you stay out of debt, build wealth, and ultimately buy the most important thing of all: complete control of your time and energy.

It all starts with gratitude

You have both been gifted with healthy bodies, along with smart and curious minds.

You are among the very privileged 15% of human beings raised in the developed world.

You have access to education, nutritious food, clean water, healthcare, and countless opportunities to participate and thrive in the largest free market the world has ever known.

Congratulations, you have won the jackpot in life’s biggest lottery.

My first bit of advice is for you to take a moment from time to time and express gratitude for all the things you do have. It makes the things you don’t have a little less important, and that’s good for your bank account. (Ok, it’s good for a lot of things, but this is a money blog, after all).

Whatever you make, it’s not as much as you think

Both of you have expressed interest in a technology career. That’s good news. Tech jobs pay well and are just about everywhere.

The average starting salary for a User Experience (UX) designer, the trending tech job these days, is a whopping $92,000 per year.

That seems like a lot of money and is probably higher than reality, but for this exercise, we will pretend that you just landed that salary straight out of college. Congratulations! I’ll email you my Christmas list.

How much do you really make?

Before you start collecting that fat $92,000 paycheck, let’s rewind back to today.

Today, you each make around $100 per month in allowance. That is your salary as a teenager. If we were your employer rather than your parents, you would only receive about $80 of that. The missing 20 bucks would be deducted to pay your social security, medicare, and income taxes.

Social security and medicare are safety-net programs to ensure you have some level of income and medical insurance when you're old. Your income tax deductions pay for a lot of things like roads, more healthcare, interest on government debt, and F-16s (pew! pew!).

In our $92,000 trendy tech job example, you would actually bring home closer to $69,000. That’s $23,000 of your money deducted from your earnings every year (about $1,900 each month) for taxes and social programs.

Some perspective

“Ok dad, $69,000, that’s not so bad!”

It’s not bad at all! In fact, it’s pretty damn amazing straight out of college.

The average starting salary for a college graduate, generally speaking, is around $52,000 per year. After social security, medicare, and income taxes, a $52K earner brings home around $42K. So unless you would like to listen to a symphony of the world’s tiniest violins, and possibly get punched in the face by one of your less-affluent friends, you should have zero complaints at this point.

It’s not retirement savings, it’s wealth building

By the time you are working in your first real job out of college, you’re probably around 23 years old.

It’s hard to get a twenty-something to think about funding retirement. That’s a world so far removed from where you are now, and maybe why 17% of you don’t sign up for your company-sponsored retirement savings plan.

“Yasss! You told me that I’m already going to fork over a lot of my hard-earned money to the tax man. I need this money way more than the future old geezer version of me.”

I understand. I was 23 once, and my biggest priority definitely wasn’t 65-year-old Allen.

Here is my advice: stop thinking of this as retirement savings, and instead think of this as wealth building.

The wealth-building power of the 401K

A 401K is basically a special kind of brokerage account that contain a bunch of mutual funds (a mutual fund is just a diversified group of “stonks”) that you can invest in and grow your money.

About 70% of companies offer a 401K. If you find yourself in the enviable position of being an in-demand tech worker, you should scratch off any shitty companies that don’t.

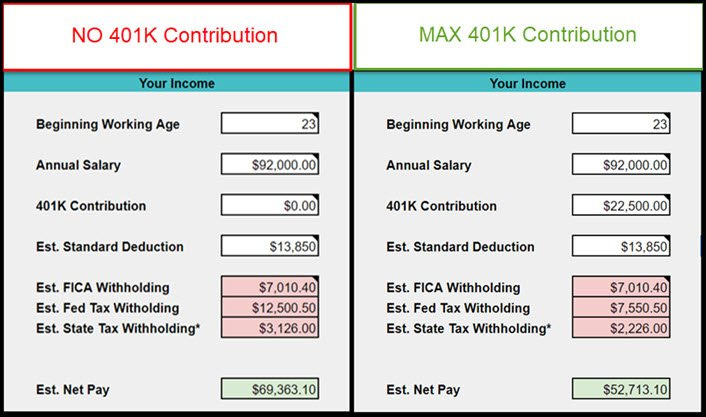

Let’s look at the impact on your Net Pay when you make the maximum contribution ($22,500) to your 401K.

On the left, we elect to just take our salary (minus taxes) with no 401K contribution. On the right, we made the maximum annual contribution of $22,500. What do you see?

“Well, my Net Pay went down from $69,363 to… wait a minute, if I contributed $22,500 to my 401K, why did my Net Pay only go down by $16,650?”

Good question! Believe it or not, the US Government wants you to save money. Social Security will not be enough to support you fully in your old age.

To incentivize you to save, 401Ks are considered tax-deferred - this means that you don’t owe taxes on any money you put into your 401K (or its investment returns) until much later.

In this example, you just deferred nearly $6,000 in taxes. Since you don’t have to pay those taxes to the government this year, that money has been added back to your take-home pay.

“Yes, but my overall take-home pay is still much lower than if I hadn’t done that.”

But you are much wealthier. Let’s look at the wealth-building impacts of making this investment:

Instead of paying $6,000 in taxes, those dollars stayed in your bank account. So even though you contributed the maximum of $22,500 to your 401K, it really only cost you about $16,500 in real dollars.

Many employers will match your 401K contributions, usually up to around 4% of your salary. For your $92,000 salary, this could mean another $3,500 or so in added wealth, bringing your 401K contribution up to around $26,000. That’s free money.

The stock market has its ups and downs, but historically, it has returned around 10% over the last century. This could mean another $2,600 in passive income added to your nest egg in its first full year, compounding higher from there.

“Compounding?”

How compounding works

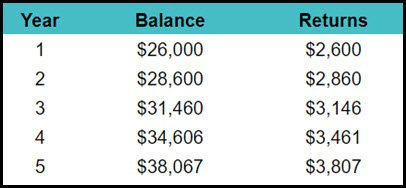

If your initial balance is $26,000, and it grows by 10%, then your ending balance would be $28,600 after one year ($26,000 + $2,600 in growth).

If your new balance of $28,600 grows by 10%, then your ending balance would be $31,460 after year two ($28,600 + $2,860 in growth).

That balance then grows by $3,146, and so on.

Notice how your growth number keeps getting bigger and bigger ($2,600 → $2,860 → $3,146). This is compounding. This is passive income. This is your money working harder and harder for you, rather than you working harder and harder for your money.

The chart below is a ridiculously simple example of how your initial $26,000 investment can grow over five years. Keep in mind that in real life, returns fluctuate. In some years, returns are higher than 10%. In other years, returns are lower or can even be negative. That’s investing.

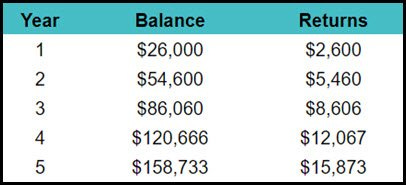

"Ok, so I invest $22,500, and my employer chips in another $3,500. So now I have $26,000 invested and that possibly grows to $38,000 in five years?”

More or less, but it gets better. You can contribute to your 401K each year, so your compounding really could look something like this:

By year five, your money could be earning you almost $16,000 per year. This is money that you don’t have to exchange your time for. Not too shabby.

Keep this up over the next twenty or so years of your career, and well…

By year 20, your portfolio could be earning more each year than your salary. Congratulations 43-year-old you, you are now financially independent.

Beware, the magic of compounding also applies to your debt in a VERY BIG WAY

When compared to your childhood allowance and part-time burger joint money, your first paycheck from your trendy hi-tech job is going to feel like a million bucks.

It’s not a million bucks. Delay that Lambo order.

Fresh out of college, you will most likely be tired of sharing an apartment with your two slobby college friends, and your car will probably leak oil and smell like cheese. A new car and an apartment in the best part of town both sound pretty good right now, especially for a highly-paid tech worker like you.

Let’s model a little lifestyle inflation into this discussion and see what happens.

Lifestyle inflation - a.k.a. “Come check out my new place! I’ll pick you up in my new car! After, we can go to this great restaurant. My treat! Oh, and then can we go to Ikea? I need new end-tables.”

For your awesome $92,000 trendy tech job, your monthly Net Pay is around $4,400 because of taxes and your excellent decision to put around $1,900 each month into your 401K.

You found an awesome studio apartment downtown for only $1,500. Your new SUV still has that new car smell. So long cheese-mobile! You spend a lot on fun activities, but your job is stressful and you deserve it.

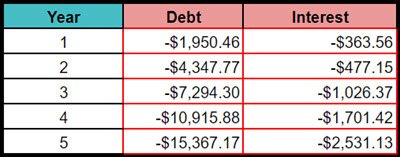

Overall, you’re just a little bit over budget each month, so that goes on the credit card. No problem, you’re still putting away nearly $1,900 each month into your 401K. Who cares about $132?

Credit cards keep you poor

Do you remember what the average returns were for the stock market over the past century?

“10%. When I’m 40, it’s gonna be Lambo time!”

Preparing you for your mid-life crisis is a topic for another blog post.

But, correct, it was 10%. And that was really cool, right? Your money would grow to a new, larger balance. Then that money would grow to a new, even larger balance. Your investments were compounding, growing larger and larger as the years go by.

Credit cards, on average, charge around 22% interest, and that compounds too… against you. Overspending and increasing your credit card balance by even a tiny $132 each month can be devastating over time.

Note: Credit card interest calculations appear complicated to your old dad; perhaps to confuse the innocent and protect the guilty. But here is a very rudimentary estimation of how debt and interest can ruin a perfectly good life.

By year 5, your debt has swelled to more than $15,000 and your interest payments alone are siphoning $2,500 from you each year.

By year 15, if you continue to overspend by $132 each month, and continue to let those balances accumulate on what is now probably a rotation of 10 or more maxed-out credit cards, your interest payments alone will cost you $33,000 per year. You will be a high-income poor person, or as they say in Texas: big hat, no cattle.

A 2011 study showed that roughly 9% of bankruptcy filers earned more than $60,000 per year ($80,000 in today’s dollars, when adjusted for inflation). Credit debt is cited as one of the top causes of bankruptcy.

When you don’t pay off a credit card in full, at 22% interest, your balance will double about every 3 years. That wagyu beef burger you bought for $45 on the credit card a few years ago? You’re still paying for it, but now it’s a $90 wagyu beef burger. In 3 more years, it will be a $180 wagyu beef burger.

Final Thoughts

Kids, this is not radical advice. It’s actually a very simple set of rules to try and live your life by.

Spend less than you make and invest the rest. Carrying credit card debt month over month will devastate your finances.

Express gratitude for the things that you do have, and be willing to wait for the things you want.

Big salaries bring big taxes; max out your 401K (if it is offered), and make sure your contributions are invested.

At age 50, when your net worth is around $3,000,000 and still compounding at 10% year over year, by all means, buy the Lambo and give your dear old dad a ride.

Best advice ever. Hope a lot of your "adult" subscribers read and take heed. I was extremely fortunate to have "Depression Era" parents who taught me sound money lessons. Unfortunately, 401k's were not something they had knowledge of and neither did I as they were new to us in the late 80's and we were thrown to the wolves in the sense of "Hey...here's your new 401K and it's up to you to learn how to make the best investment choices" with absolutely no knowledge of how to invest whatsoever. My generation was the "learning curve" for the 401k! But, my folks did teach me that we don't spend large chunks of money from your savings or lottery winnings or inheritance. You invest that money and use the interest they earn to make the payments on that new car or the European vacation. Or if you take out a bank loan for something, you not only make the scheduled payment, but you also make additional payments to the "Principal Only" so that it's paid off sooner and in the end, you've paid a little interest (but not a lot) and you still have your initial money in the bank. These loans are not to be mistaken with borrowing from your 401k....but as a regular bank loan. It's seldom a good idea to borrow money from yourself as you are essentially taking money from your account that should be earning you more but can't because you've borrowed it and the interest you pay back to yourself is rarely equal to what you would have earned on it had you never borrowed it in the first place. Anyway...I digress. You advice to your kids is Steller and I so hope they heed it.